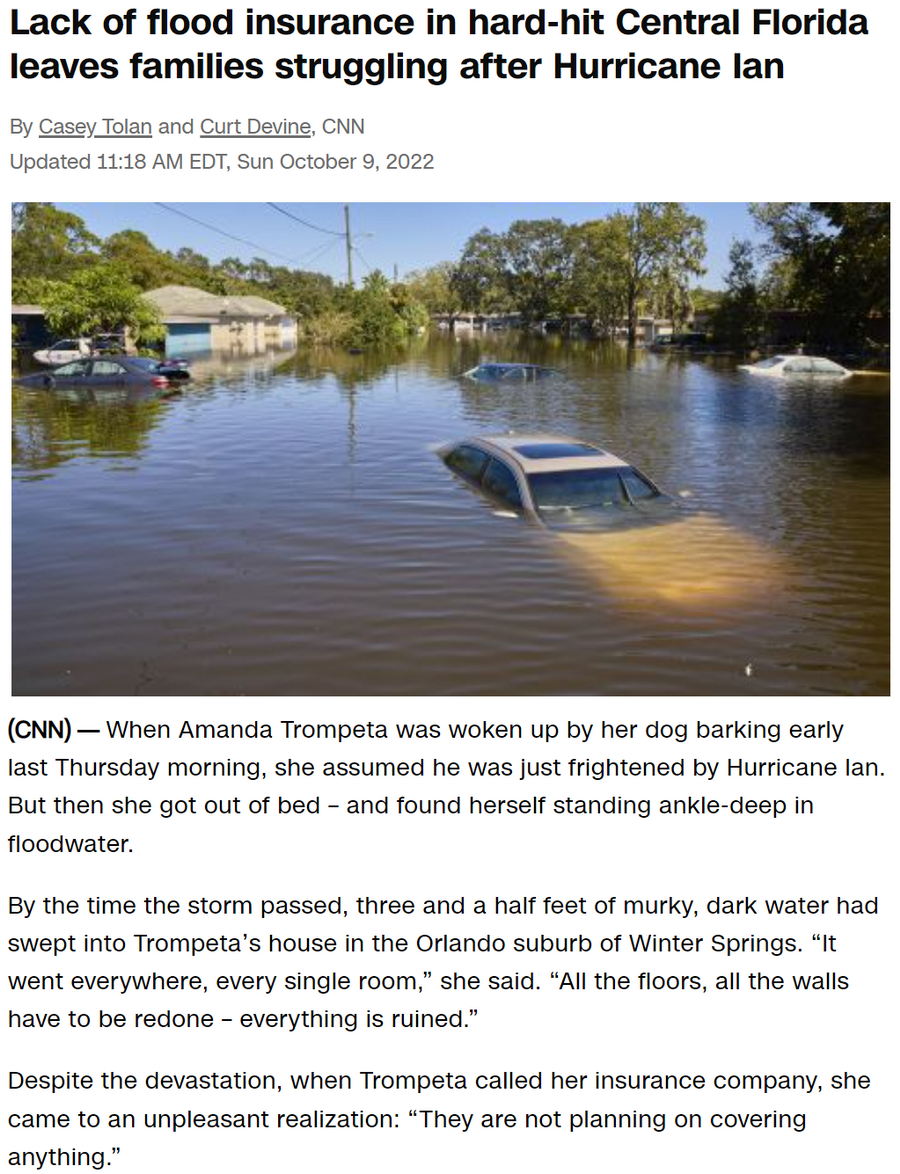

On October 9th, CNN and a few other news outlets ran with stories of families financially struggling after being flooded by their own government and their weather modification warfare, that this time was called, Hurricane Ian.

This comes as no surprise as homeowners’ insurance does not cover flood damage. You would think that it did, and most people simply assume it does, especially considering that Florida has been hit quite often by weather modification warfare such as hurricanes.

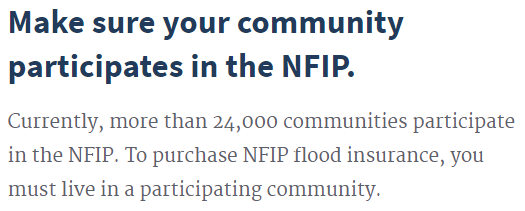

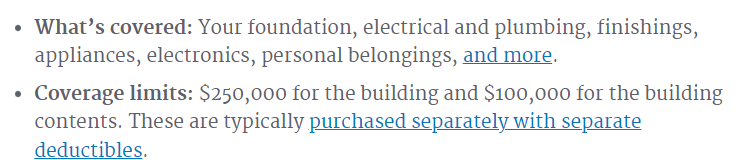

Actually, flood insurance is only available in 24,000 participating “NFIP” communities across the U.S. and is handled by FEMA and local insurance companies. To get one, you obviously must know that they exist and live in one of these communities, and then contact any of your local insurance company representatives. It’s also a minimum of a 30-day waiting period. The coverage limit is $250,000 for the building and $100,000 for the building contents. As for Florida, there is, of course, 33 available insurance providers – how very Freemasonic of them. For more information about what’s covered visit FloodSmart.gov.

Now, hiding the fact that a homeowner insurance does not cover flooding and then making it difficult to get such flood insurance is of course by design; as all these weather modification disasters are made with the goal to get people off their land – allowing the government and their corporations to buy pieces of land for pennies on the dollar. One of the main goals for Agenda 2030 is to remove ownership and the ability to be self-sufficient. Everyone should be packed into zones within smart cities where they are fully dependent on the beast system.

Also, for those only living in a house, the $250,000 limit might help. But as a homestead owner, that $250,000 limit will not go far. For businesses though, the limit is $500,000 for the building and another $500,000 for the contents. Also, I can imagine that these insurances do not come cheap, and most people would probably not be able to afford them even if they were offered.

According to the article, about a fourth of single-family homes in coastal Lee County, where Ian came onshore, are covered by federal flood insurance. The coverage rates are higher in some of the hardest-hit areas of the county, like Sanibel Island, where about half of homes are covered. But further inland, only about 4% of single-family homes in Seminole County, 3% of homes in Orange County and 2% of homes in Polk County are covered by flood insurance. All of those counties have reported significant flooding during Ian.

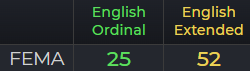

As for CNN publishing this story on October 9, it’s all in the numbers as always.

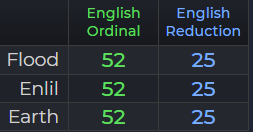

October 9 came with both a 52– and 25-date numerology, the flood- and weather modification numbers.

10/9/2022 = 1+0+9 + (20) + (22) = 52

10/9/2022 = (10) + (9) + 2+0+2+2 = 25

FEMA = 52, 25

Flood = 52, 25

Enlil = 52, 25 (Goddess of flooding)

Earth = 52, 25

Hurricane = 52

Flood Damage = 52

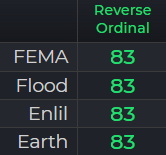

And, on October 9th, there was 83-days remaining in the year.

FEMA = 83

Flood = 83

Enlil = 83

Earth = 83

Flood Damage = 83

Society of Jesus = 83 (aka., The Jesuit Order)

Yes, the pattern of keywords is unmistakable. The perfect day for such a story. And as a bonus, this story comes at the 9th day of the month, 11 days after Ian made landfall in Florida, like 9/11, as in 911, or 11/9, as in 119.

And remember Genesis, and the verse 7:12, where the Lord made it rain for 40-days and 40-nights?

Noah and the Flood = 911

Forty Days and Forty Nights = 119

Clever bastards.